The Four Perspectives of the Balanced Scorecard

For More Information

The Four Perspectives of the Balanced Scorecard

One of the signature features of the balanced scorecard is that it looks at organizational performance from various Perspectives. Perspectives are the performance dimensions, or lenses, that put strategy in context. It takes several perspectives—usually four—to understand an organization as a system made up of elements that work together, like the gears in a clock or fine watch. Together, these elements create value, leading to customer and stakeholder satisfaction and good financial performance.

Why Does Your Organization Need Perspectives?

Drs. Robert Kaplan and David Norton found in their initial work together that too many organizations were measuring their success only from a financial point of view and that a broader, more strategic set of dimensions was needed. The success of few strategies can be measured from only one point of view. The basic four perspectives enables the organization to use a strategy map to articulate to employees how value is created by the organization.

What Balanced Scorecard Perspectives Should a Private Sector Organization Use?

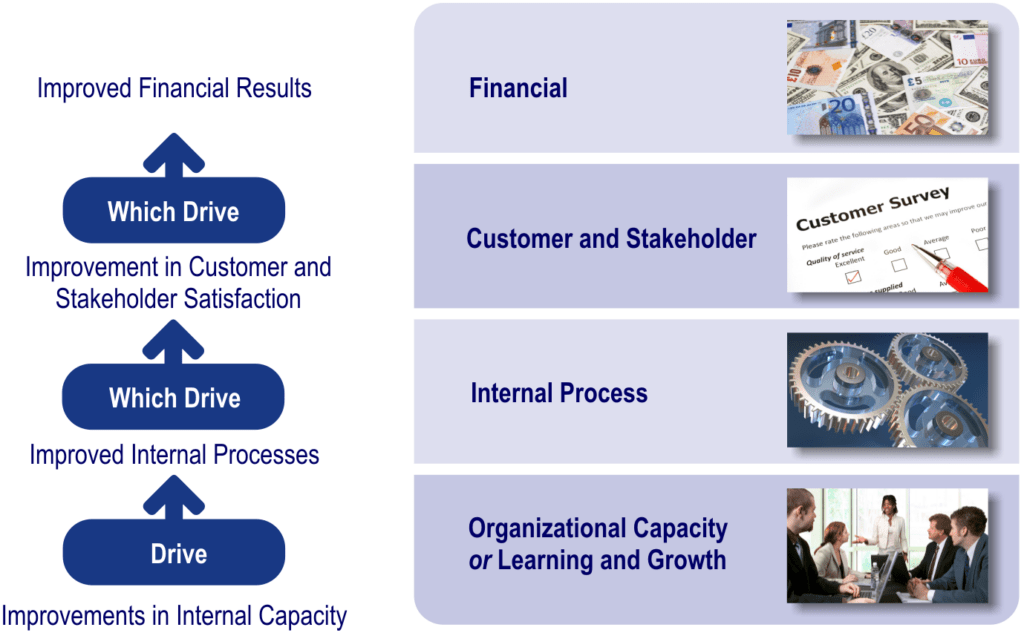

The four perspectives of a traditional balanced scorecard are Financial, Customer, Internal Process, and Learning and Growth. In the Nine Steps to Success™, the original Balanced Scorecard “learning and growth” perspective has been changed to “organizational capacity”, to reflect the internal capacity building needed to improve internal processes. The four components included in the organizational capacity perspective are human capital, tools and technology, infrastructure, and governance. Learning and growth takes place throughout the whole organization and during the execution of strategy, not just in one perspective. The image below shows the value creation story through the perspectives for business / commercial sector organizations.

How Perspectives Show a Value Creation Story in Business / Commercial Organizations

What Balanced Scorecard Perspectives Should a Public Sector Organization Use?

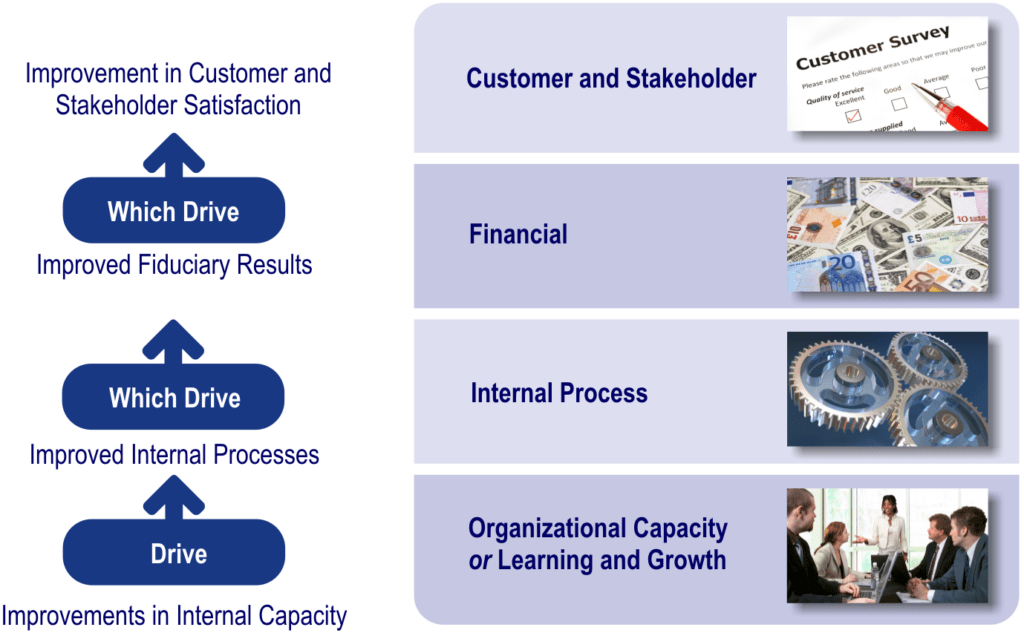

Civilian government, defense and not-for-profit organizations are mission driven. These organizations use different value-creation logic than business and industry (profit driven) organizations. In The Institute Way, mission-driven scorecard systems reflect the unique nature and value proposition of mission-driven organizations. Perspective nomenclature needs to reflect this difference. For example, governments are not in the business of making a profit, so a “financial” perspective can be a misleading way of identifying this perspective to stakeholders. “Financial stewardship” might be more appropriate, as stewardship connotes a message of wise use of (‘taxpayers’ or ‘funders’) money and fiduciary responsibility, rather than improved profitability and shareholder value. In military organizations, other government organizations and not-for-profits, terms like “resource effectiveness” or “budget effectiveness” are commonly used. For not-for-profits, financial stewardship imparts the concept of using resources cost-effectively, something donors and funders would no doubt like to see. The image below shows the high-level value-creation story through perspectives for mission-driven organizations.

How Perspectives Show a Value Creation Story in Mission-Driven Organizations

Likewise, for the customer/stakeholder perspective in the Nine Steps Methodology (as detailed in The Institute Way), words like client, member, solider and citizen are used because they emotionally tie the management system to the people or groups served by the programs and services of these mission-oriented organizations. For business and industry scorecards, the word “customers” is traditionally used to describe this perspective.

In The Institute Way, the placement of perspectives on government and not-for-profit scorecards is differentiated. Financial should not be the top perspective for a mission-driven organization’s scorecard because financial stewardship is not the end of the value chain for that type of organization—stakeholder satisfaction is the end of the value chain. For these organizations, the value chain ends not with improved business financial results (although that’s a good thing!) but with satisfied members, citizens or other stakeholders. Putting the financial (stewardship) perspective in the second position from the top is more appropriate, as stakeholder satisfaction is derived in large part by the delivery of programs and services that are cost-effective and are judged necessary and sufficient. One client used a hybrid scorecard matrix putting the financial and customer perspectives on the top row to reinforce that both financial success and customer experience were equally important results. The Nine Steps to Success™ framework is very flexible to accommodate modifications like these and still keep scorecarding principles intact.

Can I Change the Names of the Perspectives?

The perspective names can change to fit the culture of the organization, although the underlying focus typically does not. In other words, while a public sector organization might prefer the “Stewardship” label, the focus of the perspective should remain on financial performance. Choose labels that resonate with the organization’s strategy and clearly communicate internally and externally. For example, one organization might use “People and Tools” instead of “Organizational Capacity” (or “Learning and Growth”), and another might aptly describe this perspective as “People, Knowledge and Technology”.

How Do I Learn More About the Balanced Scorecard Perspectives?

Check out our Balanced Scorecard Professional Certification Program or Contact Us with questions to learn more about Perspectives or the Balanced Scorecard.

Balanced Scorecard Professional Certification

Free Articles

& White Papers

Explore Our

Strategic Planning

The Institute Way